Table of Contents >> Show >> Hide

- What a Revocable Living Trust Actually Does

- How It Works in Real Life

- Why People Set Up Revocable Living Trusts

- The Biggest Benefits of a Revocable Living Trust

- What a Revocable Living Trust Does Not Do

- Revocable Living Trust vs. Will

- What Assets Can Go Into a Revocable Living Trust?

- Who Should Consider a Revocable Living Trust?

- Common Mistakes People Make

- Experiences People Commonly Have With Revocable Living Trusts

- Final Thoughts

A revocable living trust sounds like one of those phrases people nod at during estate-planning conversations while secretly thinking, “I should probably know this, but I absolutely do not.” Fair enough. The name is formal, the topic is serious, and the paperwork can look like it was designed to frighten civilians. But the basic idea is not nearly as mysterious as it sounds.

A revocable living trust is a legal arrangement you create during your lifetime to hold and manage assets like your home, bank accounts, brokerage accounts, or other property. “Revocable” means you can change it, update it, or cancel it while you are alive and mentally capable. “Living” means it is created during your lifetime, not after death. And “trust” means the assets are managed under written instructions for your benefit now and for your chosen beneficiaries later.

In plain English, a revocable living trust is a flexible estate-planning tool that can help you stay in control while you are alive and make things easier for your loved ones after you die. It can also help if you become incapacitated, which is one reason many people like it. No cape required, but it does quietly do some hero work.

What a Revocable Living Trust Actually Does

At its core, a revocable living trust creates a legal container for your assets. You, as the person creating it, are often called the grantor, trustor, or settlor. In many cases, you also serve as the initial trustee, which means you still manage the assets as usual. You can buy, sell, invest, withdraw, and live your life without feeling like your money has been kidnapped by legal paperwork.

You also name beneficiaries, who are the people or organizations that will receive trust assets after your death. And you name a successor trustee, the person or institution that takes over if you die or become unable to manage things yourself.

That structure is what makes a revocable living trust useful. While you are alive and well, you stay in charge. If you become ill, injured, or cognitively impaired, the successor trustee can step in and manage trust assets according to your instructions. After your death, the successor trustee can distribute the trust property without sending everything through probate court first.

How It Works in Real Life

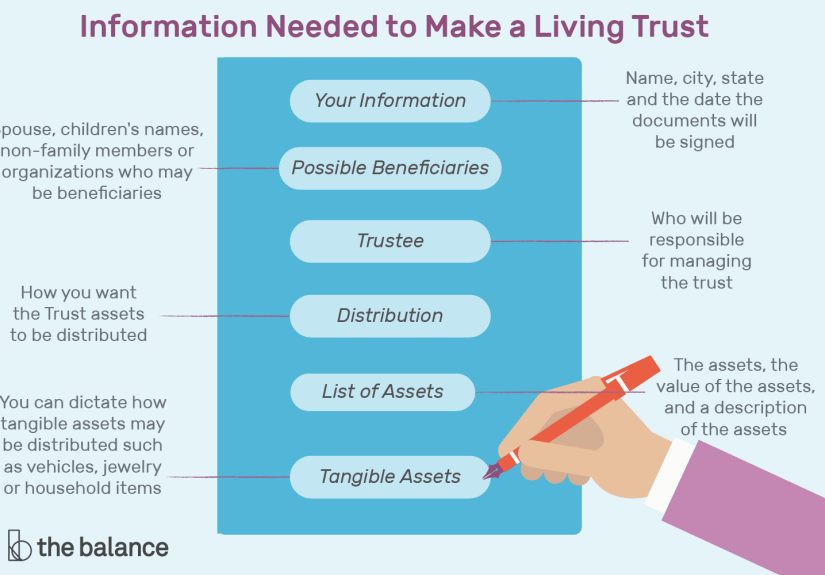

Step 1: You create the trust document

The trust document spells out the rules. It identifies the trustee, successor trustee, beneficiaries, and instructions for how the assets should be managed and distributed. You can make it simple or detailed. Some people say, “Divide everything equally among my children.” Others get more specific and say things like, “My son gets the lake house, my daughter gets the brokerage account, and nobody touches the vintage record collection unless they know how to use a turntable.”

Step 2: You transfer assets into the trust

This step is called funding the trust, and it is where the magic either happens or quietly fails. A trust only controls the assets that are actually transferred into it. If your trust exists on paper but your house, account titles, or other property are still outside it, those assets may still have to go through probate.

That means deeds may need to be retitled, bank or brokerage accounts may need to be opened or retitled in the trust’s name, and ownership records may need updating. A beautiful trust with no funded assets is a little like buying a safe and then leaving your valuables on the kitchen table.

Step 3: You review and update it over time

Because the trust is revocable, you can amend it as life changes. Marriage, divorce, remarriage, births, deaths, moves to a new state, new property, business changes, and shifting family dynamics can all be reasons to review the document. Estate planning is not a one-and-done event. It is more of a “check in before things get weird” system.

Why People Set Up Revocable Living Trusts

The biggest reason is usually probate avoidance. Probate is the court-supervised process of validating a will, gathering assets, paying debts, and distributing property. Depending on the state and the complexity of the estate, probate can be time-consuming, public, and expensive. Many people would prefer their loved ones skip that administrative obstacle course if possible.

Another major reason is incapacity planning. A will only takes effect after death. A revocable living trust can work while you are still alive. If you become unable to handle your finances, your successor trustee can manage the trust assets without waiting for a court to appoint a conservator or guardian of the estate.

People also like revocable living trusts for privacy. Probate filings are generally public. Trust administration is usually more private, which can matter if you would rather not turn your family finances into neighborhood reading material.

Finally, a revocable living trust can provide control. You can set conditions, timing, and instructions for how assets are distributed. That can be especially useful in blended families, second marriages, situations involving minor children, beneficiaries with disabilities, or adult children who are lovely but not exactly famous for restraint.

The Biggest Benefits of a Revocable Living Trust

1. It can help avoid probate for assets in the trust

This is the headline benefit. If assets are properly transferred into the trust during your life, those assets usually do not need to pass through probate at your death. That can save time and reduce legal friction for your family.

2. It can help if you become incapacitated

A successor trustee can step in and manage trust property if you cannot do it yourself. This can make bill paying, investment management, and property oversight smoother during illness, injury, or cognitive decline.

3. It offers flexibility

You can change the trust terms, swap trustees, add beneficiaries, remove beneficiaries, or revoke the trust entirely while you still have capacity. That makes it attractive for people whose lives, assets, or families may evolve over time.

4. It can keep matters more private

Unlike a probated will, a trust generally does not have to be filed publicly in court simply to function. That means fewer eyes on your assets, your beneficiaries, and your planning choices.

5. It can be useful for more complex family situations

If you want to leave assets to a surviving spouse while protecting a share for children from a prior marriage, or if you want distributions spaced out over time, a revocable living trust can provide more structure than a basic will alone.

What a Revocable Living Trust Does Not Do

This part matters because revocable living trusts are often oversold like they are legal Swiss Army knives with built-in fireworks. They are useful, but they are not magic.

It does not automatically reduce income taxes

For federal income-tax purposes, a revocable living trust is generally treated as an extension of you while you are alive. Income and deductions usually flow through to your personal tax return. In most ordinary situations, you do not create one for income-tax savings.

It does not remove assets from your taxable estate

Because you still control the assets, they are generally still considered part of your estate for federal estate-tax purposes. If someone tells you a standard revocable living trust is a secret trapdoor out of estate taxes, treat that claim the way you would treat a suspiciously cheap yacht.

It does not protect your assets from your own creditors

Since you remain in control, your creditors can usually still reach those assets. A revocable living trust is not the same thing as an asset-protection trust.

It does not replace every other estate-planning document

You may still need a will, powers of attorney, health care directives, and beneficiary designations. A trust is part of a plan, not the entire orchestra.

Revocable Living Trust vs. Will

A will and a revocable living trust often work together rather than compete for the same job. A will says who should receive your property after death and can name guardians for minor children. A revocable living trust can manage assets during your life, during incapacity, and after death.

Here is the practical difference: a will generally goes through probate, while a properly funded trust generally does not for the assets it owns. Also, if you have minor children, a will is still crucial because it is the document used to nominate guardians. A trust can help manage money for children, but it does not replace the guardian-naming function of a will.

That is why many estate plans include a pour-over will. This type of will is designed to catch assets left outside the trust and direct them into the trust at death. It is a helpful backup, but it is not a substitute for proper trust funding. If the asset was never transferred into the trust while you were alive, the pour-over will may still leave it subject to probate first.

What Assets Can Go Into a Revocable Living Trust?

Common assets that may be transferred into a revocable living trust include:

- Your home or other real estate

- Nonretirement bank accounts

- Brokerage accounts

- Business interests, depending on the entity and governing documents

- Personal property, often by assignment

- Certain intellectual property or valuable collections

Some assets require extra coordination. Retirement accounts and life insurance policies usually pass by beneficiary designation, not by simple retitling into the trust the way a house or taxable investment account might. That means your beneficiary designations should be reviewed carefully so they work with the trust instead of starting a family mystery novel after you are gone.

Who Should Consider a Revocable Living Trust?

A revocable living trust can make sense for many people, but it is especially worth considering if you:

- Own real estate in more than one state

- Want to avoid or reduce probate hassles

- Care strongly about privacy

- Want a smoother transition if you become incapacitated

- Have a blended family or more complicated beneficiary goals

- Want to stagger distributions instead of leaving a lump sum

- Own substantial property and want a more organized estate plan

That said, not everyone needs one. Some people with simple estates, modest assets, and straightforward beneficiaries may do well with a will plus beneficiary designations and powers of attorney. The right answer depends on your state law, your asset mix, your family structure, and your goals.

Common Mistakes People Make

Not funding the trust

This is the classic mistake. The trust exists, the binder is handsome, the signatures are flawless, and yet the assets never got moved. Probate then shows up anyway like an uninvited plus-one.

Forgetting to update titles and beneficiary designations

Estate planning is often less about grand gestures and more about boring accuracy. If account titles or beneficiary forms do not match the overall plan, the paperwork with the strongest legal effect may win.

Assuming the trust handles everything

People sometimes assume once the trust is signed, all estate-planning tasks are complete. In reality, you may still need a will, powers of attorney, health care documents, and regular reviews.

Never revisiting the trust

A trust written ten years ago may not reflect today’s family, property, or priorities. Review it after major life events and periodically even when life seems calm.

Experiences People Commonly Have With Revocable Living Trusts

The following examples are illustrative, based on common estate-planning situations people experience in real life.

One common experience is the couple who set up a revocable living trust after buying a second home in another state. At first, they think the trust is mostly for “wealthy people with dramatic staircases.” Then their attorney explains that owning property in more than one state can mean extra probate complications. Suddenly, the trust stops sounding fancy and starts sounding practical. They transfer both homes into the trust, update a brokerage account, and name one organized adult child as successor trustee. Years later, when one spouse dies, the survivor discovers that the trust did exactly what it was supposed to do: it reduced paperwork, avoided extra court involvement for the titled property, and made a hard season slightly less chaotic. Nobody throws a parade for paperwork that works, but maybe they should.

Another very real experience is the person who creates a trust but never funds it properly. This happens all the time. They sign the documents, feel responsible, tell everyone they are “all set,” and then forget to retitle the house or move the accounts. After death, the family learns that the trust exists but does not actually own much of anything. The result is disappointment, confusion, and often probate anyway. The lesson is not that the trust was useless. The lesson is that the funding step matters just as much as the document itself. Estate planning loves details the way toddlers love asking “why?” at bedtime. Ignore them at your own peril.

A third experience involves incapacity rather than death. Imagine an older parent who develops memory problems. Because a revocable living trust names a successor trustee, an adult daughter or son can step in to manage the trust assets, pay bills, and keep financial life moving without waiting for a drawn-out court process. Families in this situation often say the trust became valuable before anyone died. That is one of the most overlooked strengths of a revocable living trust. It is not just a “who gets what later” document. It can also be a “who keeps the lights on if I cannot manage things myself” document.

Then there is the blended-family scenario, which is where simple estate plans can get messy fast. A remarried parent may want a current spouse to live comfortably while also making sure children from a first marriage ultimately inherit certain assets. A revocable living trust can help lay out those instructions with more precision. Families in this situation often describe the trust as a way to reduce ambiguity. It cannot guarantee that everyone will suddenly become calm, saintly, and excellent at group texts, but it can reduce the legal confusion that fuels conflict.

Finally, many people report the same emotional experience after setting one up: relief. Not excitement, exactly. No one is framing their trust documents next to vacation photos. But there is often a noticeable sense of calm in knowing that someone trusted can step in if needed, that assets are organized, and that loved ones may face fewer court hassles later. Estate planning rarely feels glamorous. Still, getting a solid revocable living trust in place can feel like finally labeling the mystery keys in your junk drawer. The world is not transformed, but future-you and your family may be extremely grateful.

Final Thoughts

So, what is a revocable living trust? It is a flexible estate-planning tool that lets you manage assets during your life, change the plan as needed, prepare for incapacity, and help certain assets pass outside probate after death. It is not a tax miracle, not a creditor shield, and not a total replacement for every other planning document. But when it is properly drafted, funded, and maintained, it can be one of the most useful pieces of a thoughtful estate plan.

If your goal is to keep control while you are alive and make life easier for the people you love later, a revocable living trust is worth understanding. It may not be the flashiest document in your life, but compared with leaving a chaotic paperwork scavenger hunt behind, it is downright charming.

Note: This article is for general educational purposes only and is not legal, tax, or estate-planning advice. Estate-planning rules vary by state, and trusts should be reviewed with a qualified U.S. estate-planning attorney who can evaluate your specific goals, assets, and family situation.