Table of Contents >> Show >> Hide

- The Stronger Side: Why the U.S. Economy Still Looks Remarkably Tough

- The Weaker Side: Why So Many Americans Still Feel the Economy Is Working Against Them

- How Both Stories Can Be True at the Same Time

- What the Federal Reserve Sees in This Mixed Economy

- What to Watch Next in the American Economy

- The Bottom Line: A Two-Track Economy Is Still an Economy

- Experiences From the Split-Screen Economy

- SEO Tags

The U.S. economy in 2026 feels a bit like a split-screen movie. On the left side, employers are still hiring, consumers are still spending, and parts of business activity keep pushing forward like a marathon runner who refuses to admit the hill is steep. On the right side, inflation is still annoying, housing remains painfully expensive, small businesses are nervous, and many households feel like every trip to the gas pump comes with a tiny emotional support bill.

That is the central truth of the American economy right now: it is neither a glittering boom nor a dramatic collapse. It is resilient in some places, strained in others, and confusing almost everywhere. For investors, workers, business owners, and regular people trying to stretch a paycheck until the next one lands, “Seeing Both Sides of the U.S. Economy” means recognizing that strong headline numbers and real financial stress can exist at the exact same time.

This is not a contradiction. It is the modern American economy in full stereo. The broad picture still shows growth, jobs, and demand. But the ground-level experience can feel much shakier, especially if your rent just jumped, your grocery bill keeps freelancing upward, or you are staring at mortgage rates like they personally offended you.

The Stronger Side: Why the U.S. Economy Still Looks Remarkably Tough

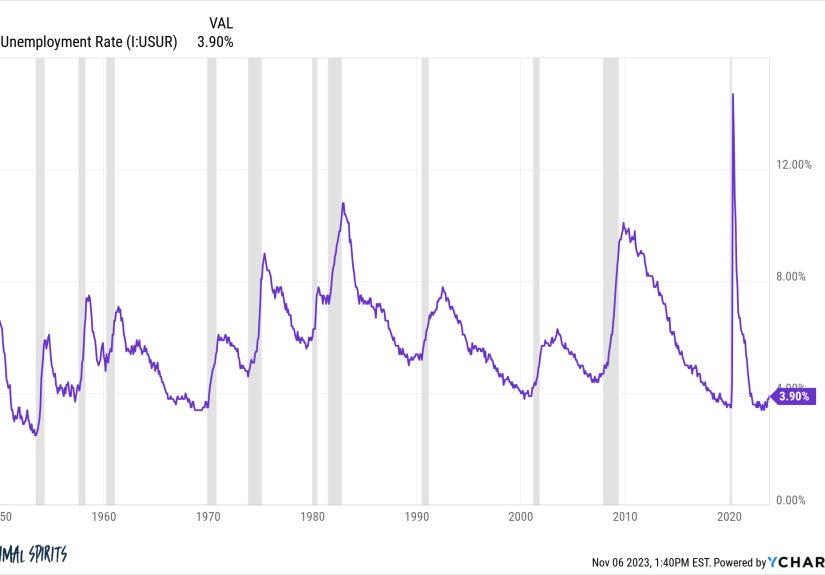

Let’s start with the good news, because there is real good news. The labor market is still holding up better than many people expected. Employers added jobs in March, the unemployment rate stayed relatively low, and wages continued to rise. Health care, construction, and transportation all posted gains. That matters because jobs are the engine that keeps everything else humming. If people are working, they are still earning. If they are still earning, they are still spending. And if they are still spending, the economy usually avoids a dramatic face-plant.

Consumer spending has also remained surprisingly steady. Personal consumption expenditures rose in February, and retail sales moved higher as well. In plain English: Americans may be grumbling, but they are still opening their wallets. Some of that spending reflects confidence. Some of it reflects necessity. Some of it probably reflects the ancient and unstoppable tradition of clicking “buy now” at 11:42 p.m. Either way, consumer activity continues to give the U.S. economy real momentum.

Business activity offers another reason for guarded optimism. The services sector, which represents a huge chunk of the American economy, remained in expansion territory in March. Manufacturing also returned to expansion, with new orders and production showing improvement. That does not mean every factory is throwing a parade, but it does suggest that parts of the goods-producing economy still have life in them.

Even broader growth has not disappeared. Real GDP growth slowed sharply in late 2025, but the full-year economy still expanded. Investment also remained part of the growth story. That matters because a healthy economy is not built on shopping alone. It also needs business spending, innovation, and productivity gains. Continued investment in technology, infrastructure, logistics, and efficiency can keep output moving even when the mood gets gloomy.

Wage growth helps, too. Earnings are still rising, which gives many households at least some cushion against higher prices. No, stronger paychecks do not magically turn a starter home into a bargain, and no one has ever walked out of a supermarket whispering, “What a wonderful deal on eggs.” Still, wage gains matter. They support household balance sheets, help people keep up with bills, and reduce the chances of a broad-based demand crash.

There is also a confidence gap between Wall Street and Main Street that is easy to miss. Many big firms continue to report stable demand, decent profits, and manageable credit conditions. Large employers generally entered this period in better shape than households did. They have more pricing power, more access to financing, and more flexibility to weather volatility. That does not mean all is well, but it does mean the business side of the economy is not uniformly fragile.

The Weaker Side: Why So Many Americans Still Feel the Economy Is Working Against Them

Now for the other side of the split screen. Inflation is still not comfortably gone. Consumer prices accelerated in March, with energy playing a major role in the jump. Core inflation remained more moderate, but the overall message was still unwelcome: the cost of living has not stopped being a problem. For households, inflation is not an abstract chart. It is a weekly reminder that the same cart somehow costs more while looking suspiciously less full.

Housing is one of the clearest examples of how the economy can look solid on paper while feeling miserable in real life. Mortgage rates remain elevated, existing-home sales have been sluggish, builder confidence has weakened, and the median home price has kept climbing. That combination is a special kind of economic irritation. Affordability has improved in some measures compared with last year, but buying a home still feels out of reach for a huge number of households. The dream of homeownership is alive; it is just currently hiding behind a monthly payment calculator.

Confidence data tells a similar story. Consumers may still be spending, but they are not exactly doing cartwheels about it. The University of Michigan’s preliminary April sentiment reading dropped sharply, showing how uneasy many households feel about prices, policy risk, and the direction of the economy. The Conference Board’s March reading showed a mixed picture, with current conditions somewhat firmer than expectations. That is a classic “today is manageable, tomorrow looks weird” signal.

Small businesses are feeling the pressure as well. The NFIB Small Business Optimism Index fell in March, and uncertainty moved higher. That matters because small businesses are often the economy’s early warning system. They feel cost pressure quickly, they notice demand shifts early, and they usually do not have a giant cash cushion sitting around like a decorative office fern. When small business owners get cautious, it often signals that the economy is becoming harder to navigate beneath the surface.

Debt is another stress point. Household debt rose to a fresh high at the end of 2025, with mortgage, credit card, auto, and student loan balances all contributing. Debt itself is not always a crisis; people borrow in healthy economies, too. But rising balances combined with higher interest costs create a tighter squeeze. A family can have a job, income growth, and still feel financially boxed in because housing, insurance, transportation, and debt service are chewing through the budget faster than the paycheck arrives.

The labor market, while still strong by historical standards, is not flawless. Job openings have cooled from their peak, hires have softened, and some sectors are clearly weaker than others. Manufacturing employment remains under pressure. Federal government employment has been declining. Long-term unemployment is up over the year. In other words, this is not the ultra-hot labor market of a couple of years ago. It is a more selective, more uneven, less forgiving hiring environment.

How Both Stories Can Be True at the Same Time

This is where people often get tripped up. They hear that unemployment is low and assume households must be thriving. Or they hear that people are upset and assume the economy must be falling apart. In reality, both impressions can be partly right.

The U.S. economy is enormous, layered, and uneven. A well-paid professional in a stable metro area may experience this economy as inconvenient but manageable. A renter with variable work hours may experience it as a daily endurance test. A homeowner with a locked-in low mortgage rate may feel wealthier thanks to rising home values. A first-time buyer may feel completely shut out. A large company may be investing in automation and artificial intelligence. A small business may be delaying expansion because every input cost feels like it came with a dare.

That is why headline data can look healthy while public sentiment looks gloomy. Aggregate statistics show the average experience. People live the marginal one. The average may say the economy is still growing. The household budget says car insurance is up, utilities are up, and chicken somehow now has a personality disorder.

There is also a timing issue. Some indicators tell you what is happening now. Others hint at what might happen next. Employment and spending often remain firm until pressure has built for a while. Confidence, housing demand, and small business expectations often weaken first. So the “good” numbers and the “bad” feelings are not necessarily fighting each other. Sometimes they are simply arriving on different schedules.

What the Federal Reserve Sees in This Mixed Economy

The Federal Reserve is basically looking at the same split-screen everyone else is seeing, except with more models, more spreadsheets, and probably less caffeine than they deserve. Policymakers have acknowledged risks on both sides of their mandate: inflation is still above target, but the economic outlook is uncertain. That is why monetary policy remains cautious.

If inflation stays sticky, the Fed has little reason to rush into easier policy. If growth slows too much or the labor market weakens materially, the pressure to cut rates grows. That balancing act matters for households because interest rates influence mortgages, auto loans, credit cards, business borrowing, and the general financial mood of the country. Right now, the message is clear: the Fed is not declaring victory, and it is not panicking either.

What to Watch Next in the American Economy

If you want to understand where the U.S. economy is headed, keep an eye on a few key themes. First, watch inflation, especially energy and core services. If prices keep running hot, consumer stress will intensify and rate relief may take longer. Second, watch employment breadth. Job growth concentrated in only a few sectors is less comforting than broad hiring across the economy.

Third, watch housing. Housing tends to magnify both optimism and pain. If mortgage rates ease and inventory improves, confidence can recover quickly. If rates stay elevated and supply remains tight, affordability will remain a drag on the broader economy. Fourth, watch consumer behavior beyond the headline spending number. Are households buying because they feel strong, or because essentials cost more? That difference matters a lot.

Finally, pay attention to business sentiment, especially among smaller firms. When small businesses pull back on hiring, inventory, and investment, the economy can lose momentum faster than the topline numbers suggest.

The Bottom Line: A Two-Track Economy Is Still an Economy

The smartest way to understand the U.S. economy right now is to stop looking for one grand, dramatic label. It is not simply “booming.” It is not simply “broken.” It is operating on two tracks at once. One track is supported by jobs, spending, business activity, and a still-resilient private sector. The other is weighed down by inflation pressure, fragile confidence, high borrowing costs, and a housing market that still feels hostile to ordinary buyers.

Seeing both sides of the U.S. economy means accepting that resilience and frustration are not opposites. They are roommates. The country can keep growing while millions of people still feel squeezed. The numbers can be respectable while the mood remains sour. The economy can be functional without feeling friendly.

And maybe that is the most American economic story of all: a system tough enough to keep going, messy enough to confuse everyone, and expensive enough to make even financially responsible adults stare at a receipt like it just betrayed them personally.

Experiences From the Split-Screen Economy

To make this more concrete, it helps to look at how this economy feels in everyday life. Consider a registered nurse in a growing metro area. She has steady work, overtime is available, and her pay is better than it was two years ago. From one angle, she is part of the economy’s success story. But rent has climbed, groceries are still pricey, and when she checked home listings in her area, the monthly mortgage payment felt like a dare from the internet. She is financially functioning, but not financially relaxed. That is one side of the U.S. economy in a nutshell.

Now picture a contractor or skilled trades worker. Construction hiring has held up, and demand for repairs, maintenance, and remodeling has not disappeared. He has a backlog of jobs and more work than he can comfortably schedule. That sounds great until materials cost more, insurance is higher, and clients hesitate before signing larger projects. His calendar is solid, but his margins are thinner. He is busy and cautious at the same time.

Then there is the small business owner running a neighborhood café, salon, repair shop, or online store. Sales may still be coming in, but not always with the same consistency. Customers are price-sensitive. Workers still expect better pay. Supplies cost more than they used to. If she raises prices, customers complain. If she does not, profits shrink. She may describe business as “fine” and mean, “I am surviving, but please do not ask me to enjoy it.” That is the emotional truth of a mixed economy.

A homeowner who locked in a low mortgage rate a few years ago experiences something totally different. His monthly housing payment is stable, home equity has increased, and he feels more insulated from rising rents than many younger households. He may look at the economy and say, “It’s not perfect, but it’s okay.” A first-time buyer hearing that comment may need a deep breath and a glass of water. For them, the same housing market looks like a velvet rope they cannot get past.

Retirees feel the divide too. A retiree with solid savings, fixed housing costs, and decent investment income may absorb higher prices without dramatic lifestyle changes. Another retiree on a tighter budget may feel every jump in food, fuel, or medical costs immediately. Same economy, different reality.

These experiences are why economic debates often feel disconnected. People are not necessarily arguing over the facts. They are reporting from different corners of the same landscape. One person sees rising wages and steady work. Another sees debt, rent, and shrinking breathing room. Both are telling the truth.

That is why “Seeing Both Sides of the U.S. Economy” matters. It reminds us that the real economy is not just a chart, a headline, or a political talking point. It is the sum of millions of lived experiences, some stable, some strained, and many stuck right in the middle.