Table of Contents >> Show >> Hide

- What a Recession Actually Means

- What Usually Breaks First

- What Happens to Regular People in the Next Recession

- What Happens to Stocks, Bonds, and Housing Markets

- What Policymakers Usually Do Next

- Why the Next Recession Could Look Different

- The Most Likely Sequence of Events

- How to Prepare Before the Next Recession Shows Up

- Conclusion: What Happens in the Next Recession?

- What a Recession Feels Like: Composite Experiences From the Ground

- SEO Tags

The next recession probably will not arrive wearing a giant name tag that says, “Hello, I am the recession.” It usually shows up more like an awkward party guest: hiring slows, layoffs start popping up in headlines, consumers get picky, businesses suddenly “reassess priorities,” and everybody begins pretending they always loved generic cereal. That is why the smartest question is not whether every economic forecast will be right. It is what usually happens when growth weakens, confidence drops, and the economy slips from expansion into contraction.

Here is the big picture: the next recession is unlikely to be a perfect rerun of 2008. It may not start in housing. It may not include a banking meltdown. It could be shorter, weirder, and more uneven, with some sectors still growing while others get walloped. But recessions still follow familiar patterns. Jobs get harder to find. Wage growth cools. credit tightens. Consumers pull back. Stocks become moody. Policymakers scramble. And households that prepared early usually suffer less than households that assumed the economy would stay sunny forever.

This guide explains what tends to happen in the next recession, why this one could look different from past downturns, and what the experience may feel like for workers, families, homebuyers, investors, and business owners.

What a Recession Actually Means

A recession is not simply “two bad quarters and everybody panics.” In practice, it is a broad decline in economic activity that spreads across the economy and lasts more than a brief wobble. That usually means weaker hiring, softer consumer spending, slower business investment, lower industrial activity, and tighter financial conditions all showing up around the same time.

In plain English, a recession is what happens when the economy stops merely coughing and starts missing work. Demand cools, production slows, incomes get squeezed, and caution spreads. One of the trickiest parts is timing: by the time the recession is officially recognized, regular people and businesses have often been feeling it for months.

That lag matters. Recessions are lived in real time but named in hindsight. So when people ask what happens in the next recession, they are really asking: what tends to break first, who feels it first, and how fast does the stress spread?

What Usually Breaks First

1. Hiring Slows Before Layoffs Become the Main Character

One of the earliest signs of a downturn is not always mass layoffs. Sometimes it is a quieter freeze. Job openings shrink. Recruiters go suspiciously silent. Employers stop replacing people who leave. Promotions get delayed. Contractors do not get renewed. New graduates discover that “entry level” somehow now requires five years of experience and the patience of a saint.

In many recessions, the first pain shows up in the labor market as hesitation rather than catastrophe. That is especially likely in a slow-burn downturn, where businesses worry about future demand but do not want to cut headcount all at once. If revenue keeps weakening, though, the mood changes. Hiring freezes become layoffs, and layoffs start hitting consumer confidence, which then makes the slowdown worse.

2. Consumers Get Choosy Fast

When people feel less secure about their jobs, they spend differently. They do not necessarily stop buying everything. They just stop buying the easy extras. Restaurant visits get trimmed. Big vacations turn into “maybe next year.” Electronics upgrades move from “treat yourself” to “the old one still turns on, technically.”

That shift matters because consumer spending drives a huge share of the U.S. economy. When households pull back, businesses lose revenue. When businesses lose revenue, they cut hours, delay hiring, or cancel expansion plans. Then households get even more cautious. Recessions love this feedback loop.

3. Business Investment Goes From Bold to Beige

During expansions, companies talk about growth, innovation, new projects, and market share. During downturns, they start using phrases like “discipline,” “optimization,” and “rightsizing,” which is corporate dialect for “the budget is in witness protection.”

Capital spending often slows in a recession. Companies delay equipment purchases, reduce travel, scale back advertising, and shelve expansion. Small businesses feel this especially hard because they usually have less room for error, thinner cash reserves, and more dependence on steady local demand.

4. Credit Gets Pickier

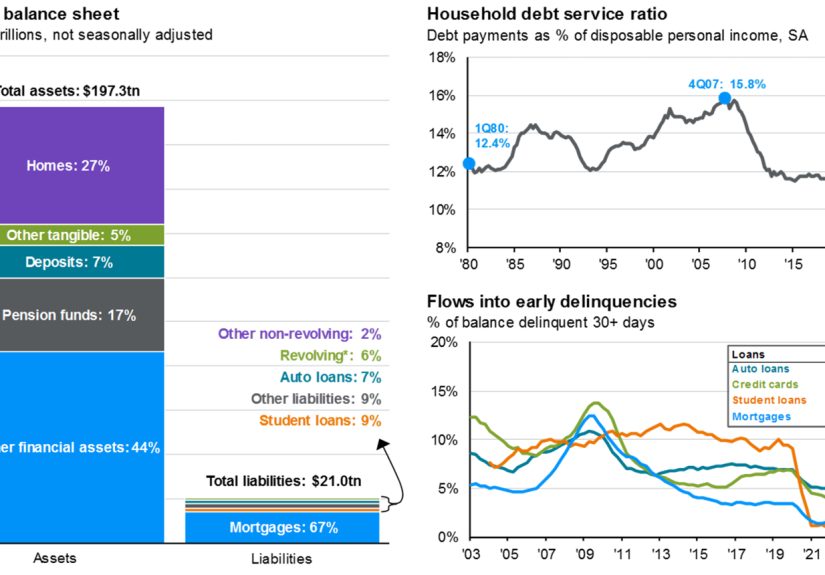

As recession risk rises, lenders get more careful. Banks may tighten standards for business loans, personal loans, credit cards, and mortgages. Even if rates fall later, access to credit can still become tougher. That means households with shaky finances and small businesses with uneven cash flow can get squeezed from both sides: income uncertainty on one side, tougher borrowing conditions on the other.

What Happens to Regular People in the Next Recession

Workers and Job Seekers

The most obvious recession effect is labor-market stress. Some people lose jobs. Many more keep their jobs but lose leverage. Raises shrink. Bonuses disappear. Overtime dries up. Switching jobs becomes harder. The emotional effect can be almost as powerful as the financial one. Even workers who remain employed often start spending like they are one bad meeting away from a budget spreadsheet crisis.

The pain is rarely evenly distributed. Construction, manufacturing, retail, hospitality, transportation, and rate-sensitive sectors often feel more pressure early. White-collar workers are not immune, especially if corporate profits weaken or companies decide technology can replace part of the payroll. The next recession could be particularly uneven if AI investment keeps some industries strong while consumer-facing or labor-heavy sectors soften.

Borrowers, Savers, and Families

Households with emergency savings usually gain something priceless in a recession: time. Time to search for work, time to avoid high-interest debt, and time to make rational decisions instead of panic decisions. Families without savings often face a harsher sequence: income shock, credit card balances, missed payments, and credit-score damage that lingers after the economy starts recovering.

High-interest debt becomes more dangerous in a downturn. If income falls while credit stays expensive, even modest balances become heavy. That is why recessions often expose problems that looked manageable in better times. A budget held together by optimism and auto-pay can unravel very quickly when hours are cut or a paycheck disappears.

Homeowners, Renters, and Buyers

Not every recession turns into a housing crash. That point deserves a marching band. The 2008 crisis trained people to think recession equals collapsing home prices, but that only happens when housing itself is the core problem or when forced selling becomes widespread.

In the next recession, housing may react more through slower sales, softer bidding wars, longer listing times, and slower price growth than through a dramatic nationwide crash. Mortgage rates could fall if the Federal Reserve cuts rates, but affordability may not suddenly become magical if lenders tighten standards or job worries keep buyers on the sidelines. Renters may still feel pressure too, especially in markets where supply is limited.

What Happens to Stocks, Bonds, and Housing Markets

Stocks Get Emotional Before the Economy Gets Officially Sad

Financial markets usually react before recession dates are stamped into economic history. Stocks tend to fall when investors expect weaker earnings, slower growth, or more uncertainty. But markets are sneaky. They often begin recovering before the economy feels healthy again. That is why investors who sell everything after the panic has already begun often manage to lock in losses with the efficiency of a professional sabotage team.

The next recession could still bring volatility, especially if the trigger involves energy prices, geopolitics, tariffs, or a sharp labor-market slowdown. But a falling market and a recession are not identical twins. Some recessions have been mild for stocks. Others have been brutal. The key point is that markets price the future, not the current mood of your group chat.

Bonds and Interest Rates May Play Defense

In a typical downturn, investors often move toward safer assets, and the Federal Reserve may cut interest rates if inflation allows. That can help bonds, cash yields, and borrowing costs over time. But there is a catch: if inflation stays sticky while growth weakens, the Fed has less room to ride in like a hero on a white horse. It may have to choose between fighting inflation and cushioning the slowdown.

That possibility matters because the next recession may not be a clean, classic demand slump. If it arrives with supply shocks, tariff pressures, or higher energy costs, policymakers could face an uglier mix than usual.

Housing Usually Slows Before It Cracks

Housing tends to feel recessions through confidence, affordability, and financing conditions. Fewer buyers qualify. Sellers adjust slowly. Builders pull back. New construction cools. Transactions fall faster than prices. In other words, the market often freezes before it breaks.

That is why the next recession could look more like a housing traffic jam than a housing cliff. People may want lower mortgage rates, but lenders may want stronger borrowers. Buyers may hope for bargains, but sellers may refuse dramatic cuts unless they are forced to move. The result can be a sluggish market rather than a cinematic collapse.

What Policymakers Usually Do Next

The Federal Reserve

If inflation is under control, the Fed typically cuts interest rates to support growth and employment. Lower rates can help borrowing, asset prices, and confidence. They do not fix everything, but they can soften the landing or shorten the pain.

If inflation remains elevated, the Fed’s job gets trickier. It may cut more slowly or wait longer, which can make the downturn feel more stubborn. That is one reason the next recession may feel frustrating rather than dramatic: the medicine might work, but not instantly.

Congress and the Federal Budget

Recessions also trigger automatic stabilizers, which is a wonderfully bland name for a very important idea. Tax revenue falls as income and profits weaken. Spending on programs like unemployment benefits tends to rise. Federal deficits usually get bigger even without brand-new legislation. Then, if lawmakers add stimulus, aid, or tax relief, deficits can rise further.

For households, this can mean a better safety net than they expected, though not always a fast or smooth one. For businesses and markets, it means government policy becomes part of the recovery story very quickly.

Why the Next Recession Could Look Different

The next recession may be shaped by forces that did not dominate earlier downturns in quite the same way. AI investment could keep parts of the economy humming even while hiring weakens elsewhere. Lower immigration may change what “normal” job growth looks like. Tariffs or geopolitical shocks could pressure prices even as demand softens. High federal debt may limit political appetite for huge stimulus, even if the economy weakens.

That means the next recession might be less like a universal collapse and more like a patchwork slowdown. Some industries may still post strong profits. Some regions may look fine. Some households may feel little immediate pain. Others may feel like the floor gave way months before the official recession call. In short, the next downturn could be selective, confusing, and very uneven.

The Most Likely Sequence of Events

- Growth softens. Consumers get cautious, business investment weakens, and hiring slows.

- Confidence falls. Markets wobble, headlines darken, and companies become more defensive.

- Layoffs rise. Not everywhere at once, but enough to damage spending and morale.

- Credit tightens. Lenders become more selective, making it harder to borrow through the slump.

- Policy response begins. The Fed, Congress, or both step in depending on inflation and politics.

- Recovery starts before it feels obvious. Markets often improve first, then hiring, then consumer confidence.

That last point is important. The economy usually begins healing before most people trust the recovery. Recessions end statistically before they end emotionally. The vibes remain terrible long after the charts stop screaming.

How to Prepare Before the Next Recession Shows Up

- Build cash reserves. An emergency fund buys time, flexibility, and better choices.

- Reduce expensive debt. High-interest balances become nastier when income gets uncertain.

- Protect employability. Keep your resume current, strengthen your network, and learn skills that travel well.

- Avoid panic investing. Volatility is normal; making permanent decisions based on temporary fear is not.

- Stress-test your budget. Figure out what you would cut first if income fell for three to six months.

- Be realistic about housing. Lower rates do not always mean easier approvals or lower total costs.

The goal is not to predict the exact month of the next recession. Good luck with that. The goal is to become harder to knock over when the cycle turns.

Conclusion: What Happens in the Next Recession?

In the next recession, the economy will probably not collapse in one dramatic movie scene. It will more likely slow in stages. Hiring will weaken. Some layoffs will follow. Consumers will become choosier. Businesses will delay plans. Credit will get fussier. Markets will swing wildly between dread and relief. Policymakers will respond, though perhaps less cleanly than everyone hopes. Some sectors will hurt badly, others will muddle through, and the recovery will likely begin before it feels emotionally convincing.

That is the essential truth about recessions: they are painful, but they are also cyclical. They expose weak balance sheets, punish overconfidence, and reward preparation. The next downturn may be unusual in its trigger and uneven in its effects, but the human experience will still feel familiar. People will worry about jobs, spending, debt, housing, and the future. People will adapt. And eventually, the economy will expand again, while everyone claims they totally saw it coming.

What a Recession Feels Like: Composite Experiences From the Ground

The following examples are composite, reality-based experiences drawn from common patterns seen in past U.S. downturns. They are not fictional prophecy; they are practical portraits of how recession stress tends to show up in everyday life.

The New Graduate

You finish school expecting a messy but manageable job hunt. Instead, listings disappear, interviews stretch for weeks, and companies suddenly decide to “pause hiring until next quarter.” Your friends are all posting motivational quotes on LinkedIn with the haunted energy of people trying not to scream. You take freelance work, a part-time role, or a job outside your field just to keep moving. The hardest part is not only the money. It is the uncertainty. You start questioning your timing, your degree, and your sanity, even though the problem is bigger than you. In many recessions, young workers absorb outsized damage because employers can delay entry-level hiring without shutting down operations.

The Mid-Career Employee

You still have a job, which should feel reassuring, but the mood at work changes. Travel freezes. Budgets shrink. Open roles disappear. Leadership starts talking about “efficiency,” and nobody likes that word anymore. Your annual raise is tiny. Your bonus vanishes. You do the work of two people because the team that was supposed to grow is now somehow “lean by design.” You spend less, save more, and refresh your resume after dinner like it is part of your nightly skincare routine. This is one of the most common recession experiences: not job loss, but job anxiety mixed with smaller financial gains.

The Household With a Mortgage

You own a home, so people assume you are safe. Maybe you are safer, but not stress-free. If one income weakens, the mortgage suddenly feels much larger. You stop nonessential spending, postpone repairs, and quietly hope nothing expensive starts leaking, breaking, or exploding. If rates fall, refinancing sounds appealing, but qualifying may not be easy if your income is less stable. If you wanted to move, you may stay put because the market feels sluggish and uncertain. A recession does not always crush homeowners through falling prices. Sometimes it traps them in caution.

The Small Business Owner

Revenue does not collapse overnight. It just gets softer and less predictable. Customers delay purchases. Suppliers still want to be paid. Borrowing feels more expensive or harder to access. You cut inventory, pause hiring, reduce marketing, and start doing mental math at 2:00 a.m. for sport. You may survive, but only by becoming more conservative than you wanted to be. That restraint then feeds the broader economy: fewer hires, fewer orders, fewer investments. Small businesses often experience a recession as a rolling squeeze rather than a single dramatic blow.

The Long-Term Investor or Retiree

Your portfolio falls, headlines get uglier, and every financial pundit suddenly sounds like they are narrating the end of civilization. If you have cash reserves and a plan, you can ride it out. If you need to sell assets to cover near-term expenses, the downturn feels much more personal. Retirees especially feel the sequencing risk: bad market timing hurts more when withdrawals are already underway. The emotional challenge is enormous. The temptation to “wait until things feel better” is everywhere, even though markets often recover while the news still sounds awful. Recessions test discipline as much as they test wealth.