Table of Contents >> Show >> Hide

- Loan Term, Defined (In Plain English)

- Why Loan Term Matters More Than People Think

- Loan Term vs. Interest Rate vs. APR (Yes, They’re Different)

- Loan Term and Amortization: The Payment Story Arc

- How Loan Term Changes Your Payment and Total Cost (With Real Numbers)

- Typical Loan Terms by Loan Type

- When the Loan Term Isn’t the Whole Story

- How to Choose the Right Loan Term for You

- Loan Term Red Flags to Watch For

- FAQ: Quick Answers About Loan Terms

- Conclusion: The Loan Term Is Your Financial Timeline

- Real-World Loan Term Experiences (Composite Stories)

- 1) The “I chose the longest term because it looked comfy” auto loan

- 2) The “15-year mortgage looked scary… until the math showed up” moment

- 3) The personal loan that fixed today but haunted tomorrow

- 4) The “balloon payment surprise” that wasn’t actually a surprise (it was just ignored)

- 5) The refinance decision: shorter term, same payment

If you’ve ever shopped for a loan and felt like you were suddenly majoring in “APR Studies” with a minor in “Fine Print,” you’re not alone.

One of the most important (and most misunderstood) phrases you’ll see is loan term.

It sounds like something you’d memorize for a quizyet it can quietly decide whether your monthly payment feels like a gentle breeze or a gusty hurricane.

In this guide, we’ll break down what a loan term is, how it affects your payment and total cost, how it differs from things like interest rate and APR,

and how to pick a term that fits your lifewithout turning your budget into a suspense novel.

Loan Term, Defined (In Plain English)

A loan term is the length of time you agree to take to repay a loan.

In other words, it’s your repayment timelinethe number of months or years between “Here’s the money” and “We’re done here.”

Loan terms are usually stated in months (like 36, 60, or 84 months) or years (like 15 or 30 years).

The term is a core part of your loan agreement because it shapes how your debt gets paid downand how much it costs along the way.

The big idea: loan term influences your monthly payment, your total interest cost, and sometimes even your interest rate.

Longer terms can make monthly payments smaller, but they often increase the total interest you pay over the life of the loan.

Shorter terms usually do the opposite: bigger monthly payments, but less total interest.

Why Loan Term Matters More Than People Think

When you’re comparing loans, it’s tempting to focus only on the monthly payment (“Look! I can afford it!”).

But the loan term is the behind-the-scenes director controlling that monthly numberand the final price tag.

1) Your monthly payment

Generally, a longer term spreads repayment out across more months, so each payment can be smaller.

A shorter term compresses repayment into fewer months, so payments tend to be higher.

2) Your total interest paid

Interest is typically charged based on your balance over time. The longer you carry a balance, the more chances interest has to show up and do its thing.

That’s why longer-term loans often cost more overalleven if the payment looks friendlier.

3) Your interest rate (sometimes)

Depending on the type of loan and your credit profile, shorter terms can sometimes come with lower rates.

Lenders may view a shorter repayment window as less risky.

4) Your financial flexibility

A longer term can help cash flow today, but may keep you in debt longerreducing flexibility later.

A shorter term can free you faster, but only if the higher payment doesn’t strain your budget.

Loan Term vs. Interest Rate vs. APR (Yes, They’re Different)

Loan shopping has a few terms that sound like they’re in a band together. Here’s how to tell them apart:

Loan term

The time you have to repay the loan (for example, 60 months or 30 years).

Interest rate

The cost of borrowing expressed as a percentage. This rate helps determine how much interest you pay.

APR (Annual Percentage Rate)

APR is a broader measure of borrowing cost than the interest rate because it can include certain fees and charges in addition to interest.

That’s why APR is often higher than the interest rate.

Quick takeaway

Loan term tells you “how long,” interest rate tells you “how pricey,” and APR tells you “how pricey once you include certain fees.”

When comparing loans, looking at both APR and term helps you compare apples to apples (not apples to “surprise fees”).

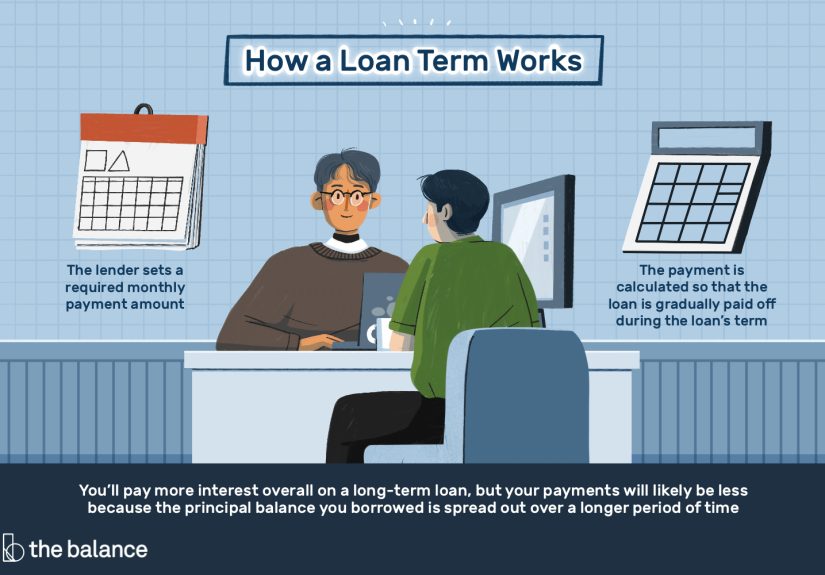

Loan Term and Amortization: The Payment Story Arc

Many common loanslike mortgages, auto loans, and personal loansare amortizing loans.

That means you make regular payments and gradually pay down both interest and principal.

An amortization schedule is a chart that shows how each payment is split between interest and principal over time.

Early on, a larger share often goes to interest; later, more goes toward principal.

This can feel unfair at first (“Why am I paying so much and my balance barely moves?”), but it’s how amortization typically works.

This matters for loan term because a longer term usually means more payments, and therefore more time for interest to accumulate.

A shorter term means fewer payments and less time carrying a balance.

How Loan Term Changes Your Payment and Total Cost (With Real Numbers)

Let’s use simple examples to show how term length changes what you pay.

These are illustrationsactual rates and offers vary by lender, loan type, and your credit.

Example 1: Auto loan term (60 months vs. 84 months)

Suppose you borrow $20,000 at 7% APR:

- 60-month term: about $396.02/month, total interest about $3,761.44

- 84-month term: about $301.85/month, total interest about $5,355.70

The 84-month option saves you roughly $94/month, which can feel like a win in the short run.

But it costs about $1,594 more in total interest over the life of the loan.

That “lower payment” is realbut it often comes with a “higher total cost” sidekick.

Example 2: Mortgage term (30 years vs. 15 years)

Now imagine a $300,000 mortgage at 6.5% APR:

- 30-year term: about $1,896.20/month, total interest about $382,633.47

- 15-year term: about $2,613.32/month, total interest about $170,397.98

The 15-year term raises the monthly payment by about $717, but it can reduce total interest by roughly $212,235.

That’s not pocket changethat’s “buy a whole additional house in some timelines” money.

Bottom line: a longer loan term can improve monthly affordability, but it often increases your total cost.

A shorter term can reduce interest dramatically, but only works if the higher payment fits your budget comfortably.

| If you choose a… | Monthly payment | Total interest | Debt-free sooner? | Common use case |

|---|---|---|---|---|

| Shorter term | Higher | Lower | Yes | Paying less overall, building equity faster |

| Longer term | Lower | Higher | No | Keeping payments manageable, cash flow focus |

Typical Loan Terms by Loan Type

Loan terms vary a lot depending on what you’re borrowing for. Here are common ranges you’ll see in the U.S. marketplace:

Mortgage loan term

Many mortgages are offered in 15-year, 20-year, or 30-year terms.

Shorter mortgage terms often build equity faster and reduce total interest, while longer terms usually lower monthly payments.

Auto loan term

Auto loan terms commonly fall in the 36–84 month range, and longer terms can exist.

The market has trended toward longer auto loans in recent years, which can lower payments but may raise the risk of owing more than the car is worth (negative equity).

Personal loan term

Many personal loans are structured around terms such as 2 to 7 years (though longer terms can appear).

Term choice often becomes a balancing act between an affordable monthly payment and minimizing total interest.

Student loan repayment period

Federal student loan repayment periods can vary by plan, commonly spanning 10 to 30 years.

Your plan (standard, extended, income-driven options, consolidation) can change the timeline.

Credit cards and revolving credit

Credit cards usually don’t have a “loan term” in the traditional sense because they’re revolving credit:

you can borrow, repay, and borrow again up to a limit. Instead, the key concept is how quickly you pay the balance off.

When the Loan Term Isn’t the Whole Story

Even if your contract says “60 months,” real life has a way of remixing plans. A few features can change your effective loan timeline:

Extra payments (prepayment)

Paying extra toward principal can shorten your payoff timeline and reduce total interest.

But some loansespecially certain mortgagesmay include a prepayment penalty, a fee charged for paying off the loan early.

If you’re the type who likes to “accidentally” pay off debt faster, check the fine print.

Refinancing

Refinancing replaces your existing loan with a new one.

People refinance to lower the interest rate, change the monthly payment, switch between fixed and adjustable rates, or alter the loan term.

A refinance can shorten your term (pay off faster) or extend it (reduce payments).

Balloon payments

Some loans have lower regular payments but end with a large, lump-sum final payment called a balloon payment.

Balloon structures can come with shorter terms, and they require planningbecause the last payment can be massive.

Deferment, forbearance, or payment pauses

Some loan programs allow temporary pauses or reduced payments during hardship.

While these tools can help in a pinch, they may extend how long you’re paying and can increase total cost depending on how interest accrues.

How to Choose the Right Loan Term for You

The best loan term isn’t “shortest” or “longest.” It’s the one that fits your goals and your budget without stress-testing your nervous system.

Here’s a practical way to decide:

Step 1: Start with your budget (and be honest)

Pick a monthly payment that leaves room for real life: groceries, gas, rent, emergencies, and yesfun.

If your payment choice requires perfect behavior for the next five years, it’s not a plan; it’s a wish.

Step 2: Compare total cost, not just the monthly payment

Ask: “How much will I pay in total interest over this term?” A lower payment can hide a higher lifetime cost.

If two terms both fit your budget, the shorter one may cost less overall.

Step 3: Think about the asset you’re buying

- Cars depreciate. Very long auto loan terms can raise the risk of negative equity.

- Homes often appreciate over time (though not guaranteed). Longer terms can boost affordability, but add interest cost.

- Personal loans often cover expenses that don’t “grow” in value. Longer terms may keep you paying for yesterday’s purchase.

Step 4: Check for flexibility and penalties

Can you make extra payments without fees? Is there a prepayment penalty? Are there balloon payments?

The “best” term on paper can become less appealing if the loan punishes you for paying it off early.

Step 5: Stress-test your future self

Imagine your income drops, or expenses rise, or life throws a surprise plot twist.

Would the payment still be manageable? If not, a slightly longer term might be safer.

If yes, a shorter term could save you serious money.

Loan Term Red Flags to Watch For

Not all “terms” are created equal. Watch for these issues when reviewing loan documents:

Balloon payments you weren’t expecting

If your loan doesn’t fully pay down by the end and requires a big final payment, you need a plan for that day.

“I’ll figure it out later” is not a plan. It’s a sitcom premise.

Prepayment penalties

A fee for paying early can reduce your ability to refinance or pay off faster.

If you want flexibility, look for loans that allow prepayment without penalty.

Very long terms on fast-depreciating assets

Long auto loan terms may lower monthly payments, but they can increase the chance you owe more than the car is worth,

especially early in the loan. That can complicate selling, trading in, or dealing with a totaled vehicle.

Adjustable rates without a clear “worst-case” plan

If the rate can rise, your payment can rise. Make sure you understand how often the rate adjusts and what the cap is.

A loan term isn’t just timeit’s time plus risk.

FAQ: Quick Answers About Loan Terms

Is the loan term the same as the repayment period?

In many consumer-loan contexts, yesboth refer to how long you have to repay.

You may also see the term “maturity date,” which is the date the loan is scheduled to be fully repaid.

Does a longer loan term always mean a higher interest rate?

Not always, but it can happen. Some lenders price longer terms higher because there’s more time for risk to show up.

Even when the rate is the same, a longer term often increases total interest because you pay interest for more months.

Can I change my loan term after I sign?

Typically, you can’t change the original term without modifying the loanusually through refinancing.

However, you can effectively shorten the term by paying extra (if your loan allows it without penalties).

What’s better: the lowest payment or the shortest term?

The “best” option is the one that fits your budget while keeping total cost reasonable.

If a short term makes you payment-stressed, it may backfire. If a long term keeps you in debt forever, it may also backfire.

The sweet spot is affordable payments with a timeline you can live with.

Conclusion: The Loan Term Is Your Financial Timeline

A loan term is more than a number of monthsit’s a commitment about how long you’ll carry a balance, how much you’ll pay each month,

and how much interest you’ll hand over in total.

The shortest term often minimizes interest, but only if the payment doesn’t squeeze your budget.

The longest term often maximizes breathing room, but can raise total cost and keep you paying long after the excitement of buying something has faded.

When you compare loans, don’t just ask, “Can I afford this payment?” Also ask:

“How much will this cost me overall?” and “Will future-me still be happy with this decision?”

Future-you deserves nice thingslike options.

Real-World Loan Term Experiences (Composite Stories)

Below are common loan-term “life moments” borrowers often run into. These are composite examples (not real individuals),

but they’re realistic snapshots of how loan term decisions play out.

1) The “I chose the longest term because it looked comfy” auto loan

A buyer focuses on the monthly payment and signs an 84-month auto loan because it makes the budget feel relaxed.

For the first year, everything is fineuntil the car needs new tires and the buyer considers trading it in.

The trade-in offer is lower than expected (cars depreciate quickly), and the loan balance is still high because amortization is slow early on.

The result: negative equity. The buyer learns that a longer loan term can make it easier to buy the car,

but harder to sell it or pivot later.

2) The “15-year mortgage looked scary… until the math showed up” moment

A homeowner compares a 30-year mortgage with a 15-year option. The 15-year payment is higher, and at first it feels like a deal-breaker.

But after budgeting and trimming a few recurring expenses, the homeowner realizes the payment is doable.

Seeing the difference in total interest is the turning point: the shorter term could mean paying dramatically less overall.

The homeowner chooses the shorter term and treats the higher payment like a forced savings planbuilding equity faster.

3) The personal loan that fixed today but haunted tomorrow

Someone uses a personal loan to consolidate credit card balances. A long term makes the payment manageable, which helps immediately.

But after a year, the borrower notices something: the loan is still hanging around, and the total interest is higher than expected.

The lesson isn’t “long terms are bad.” It’s that long terms are best used intentionallyespecially for debt consolidation.

If the budget allows, increasing payments or choosing a shorter term can reduce the overall cost.

4) The “balloon payment surprise” that wasn’t actually a surprise (it was just ignored)

A borrower signs a loan with low monthly payments and barely thinks about the balloon payment at the end.

Years later, the final lump sum arrives like a calendar invite from the past. Panic follows.

The borrower scrambles to refinance or sell the asset, and learns an important rule:

if a loan term ends with a balloon payment, your plan for the balloon should begin on day onenot on the due date.

5) The refinance decision: shorter term, same payment

A homeowner refinances when rates drop and keeps the monthly payment about the samebut switches to a shorter term.

Instead of “saving” money monthly, the borrower uses the improved rate to accelerate payoff.

This strategy can feel less flashy than lowering the payment, but it can reduce the total interest and shorten the debt timeline.

The key experience here is that loan term decisions aren’t one-time choices; they can be revisited when your income, goals, or interest rates change.

If there’s a shared theme in these experiences, it’s this: your loan term should match your actual life,

not an imaginary version of you who never has unexpected expenses, never changes jobs, and never needs a financial backup plan.

Choose a term that keeps you stable, then use extra payments (when possible) to speed things upon your terms.