Table of Contents >> Show >> Hide

- What an “All-Time High” Actually Means (and Why It Freaks Us Out)

- The Core Idea: Record Highs Don’t Arrive One at a Time

- Why More Highs Happen After Highs

- The Big Trap: “I’ll Invest After the Next Dip”

- Reality Check: More Highs Doesn’t Mean “No Drops”

- So What Should You Do When the Market Is at an All-Time High?

- Two Practical Examples (Because Advice Is Easier When It’s Not Abstract)

- Frequently Asked Questions

- Conclusion: The Market Keeps Setting Records Because Progress Keeps Happening

- Experiences at All-Time Highs: What It Actually Feels Like (and What People Learn)

- Research Basis (No Links, Just the Reputable Sources Used)

The stock market hits an all-time high and suddenly everyone turns into a part-time detective. “Is this the top?” “Should I wait for a pullback?”

“Why does my brain insist on buying groceries after I’ve already eaten?”

If you’re feeling that familiar mix of FOMO and dread, you’re not alone. Record highs can feel like a party where you show up late and assume the chips are gone,

the music is about to stop, and someone’s going to ask you to help clean up. But here’s the punchline that long-term data keeps delivering:

all-time highs are often followed by… more all-time highs.

That doesn’t mean the market never drops after a record (it absolutely can). It means a record high is not a “game over” screen. Most of the time, it’s just

what an upward-trending market does on its way to the next milestone.

What an “All-Time High” Actually Means (and Why It Freaks Us Out)

An all-time high is simply the highest level an index (like the S&P 500) has ever reached, often measured by a closing price.

It’s not a prophecy. It’s not a guaranteed cliff. It’s a new point on a chart that has spent decades leaning upward.

The emotional problem is that humans are wired to treat “highest ever” like “most dangerous.” In nature, that’s sometimes true.

In markets, it’s more complicatedbecause markets set “highest ever” levels repeatedly when the long-term trend is positive.

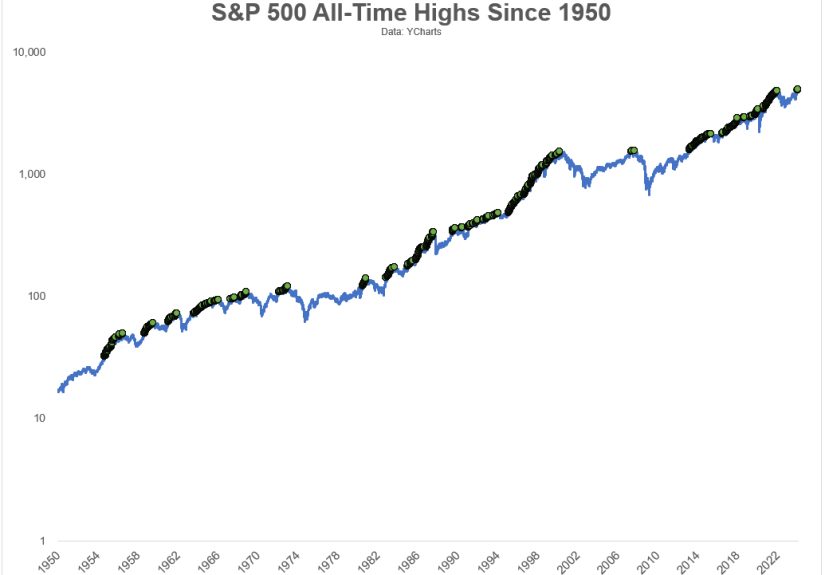

The Core Idea: Record Highs Don’t Arrive One at a Time

One of the most useful “de-spookifying” insights from long-run S&P 500 history is that new highs tend to cluster.

When the market is in a strong uptrend, it sets a record, then sets another, then anotherlike it’s trying to earn a loyalty card reward.

In other words: record highs are often a feature of bull markets, not a warning label that one has expired.

If the market rises over time, it must keep making new highs. That’s not optimism; it’s math.

Why More Highs Happen After Highs

1) Corporate earnings generally grow over time

Stocks are ownership stakes in businesses. Over the long haul, many businesses expandselling more, improving productivity, raising prices with inflation,

launching new products, and finding new customers. Earnings growth doesn’t move in a straight line, but the long-run direction has historically been up.

2) Inflation quietly pushes “nominal” prices higher

Inflation is annoying at the gas pump, but it also means that the dollar value of assets, revenues, and profits tends to drift higher over multi-year periods.

This is one reason why “the market is at a record!” is an evergreen headline. Time passes. Prices rise. Records fall.

3) Trends can persist longer than your nerves can tolerate

Markets are messy in the short term, but trends do exist. When investor expectations improve, financial conditions loosen, and earnings surprise to the upside,

risk assets can keep climbing. This persistence is also why waiting for “the perfect entry” can turn into a multi-year hobby.

The Big Trap: “I’ll Invest After the Next Dip”

This plan sounds responsible, like meal-prepping or reading the terms and conditions. In practice, it often goes like this:

you wait for a dip, the market keeps rising, you wait harder, then you finally buy after it’s gone up another 12% because you can’t take it anymore.

Congratulationsyou’ve invented “buy high, buy higher.”

The deeper issue is that market timing requires being right twice: when to get out (or stay in cash) and when to get back in.

Most people don’t miss the gains because they’re bad at math; they miss them because they’re human.

The “Best Days” Problem (aka: Why Timing Is So Brutal)

Some of the market’s strongest up days happen near some of its worst down days, often during turbulent periods.

That means if you step out to avoid pain, you might also miss the rebound that does most of the repair work.

It’s not just theory. Multiple long-horizon illustrations from major financial firms show that missing only a handful of top-performing days

can dramatically reduce long-run results. And because those best days tend to arrive unpredictablyoften when headlines are scariestpeople are least likely

to be fully invested when they happen.

Reality Check: More Highs Doesn’t Mean “No Drops”

Let’s not turn this into a fairy tale where the market floats upward like a balloon that never meets a cactus.

Corrections (commonly defined as drops of 10% or more) happen. Bear markets happen. Recessions happen.

Sometimes the market hits a new high and then faceplants for a while.

The point isn’t that risk disappears at record highs. The point is that record highs alone are not a reliable signal of imminent disaster.

If you’re investing for a goal that’s 10, 20, or 30 years away, the market is going to hit many records along the way.

Treating each one like a fire alarm is exhaustingand often expensive.

So What Should You Do When the Market Is at an All-Time High?

1) Keep your process boring on purpose

Boring beats brilliant. Automatic investing (weekly, biweekly, or monthly) turns “Should I buy now?” into “It’s Tuesday.”

This approach is commonly known as dollar-cost averaging when you invest a consistent amount at regular intervals.

It won’t prevent losses, but it can reduce the emotional load of trying to pick perfect moments.

2) Match your risk to your time horizon

Money you need next year should not be auditioning for the role of “stock market hero.” Short time horizons and high stock exposure can be a rough combo.

But long-term goals (retirement, a child’s future education, long-range wealth building) can generally tolerate volatility betterbecause they have time.

3) Diversify like you mean it

A headline index can hide concentration risk. If a handful of mega-companies dominate returns, portfolios that look diversified on paper may be less balanced than you think.

Diversification across sectors, styles, and (where appropriate) international markets can help reduce the “one narrative to rule them all” problem.

4) Rebalance instead of “predict”

Rebalancing is the grown-up version of “buy low, sell high.” If stocks surge and become a larger slice of your portfolio than intended,

rebalancing trims some exposure and restores your plan. If stocks drop, rebalancing can nudge you to add when it feels uncomfortable.

It’s a rules-based way to respond to volatility without pretending you can forecast the next headline.

5) Keep expectations realistic

It’s completely possible for stocks to make new highs and still deliver more muted returns over the next decade compared with the past.

Valuations, interest rates, and earnings growth all matter. Some major investment research teams have recently published more conservative

long-term return assumptions for U.S. stocks than the historical average.

Translation: you can believe “highs can lead to more highs” while also planning for a world where future returns may be less explosive

and where diversification and savings rate matter even more.

Two Practical Examples (Because Advice Is Easier When It’s Not Abstract)

Example 1: The “Waiting for a Dip” investor

Maya has $10,000 ready to invest. The market is at a record. She decides to wait for a 10% drop “to be safe.”

But the market rises another 12% over the next year before any meaningful pullback happens. She finally buysat a higher pricebecause

staying in cash feels like watching a train leave the station in slow motion.

Maya wasn’t irrational. She was responding to uncertainty. The issue is that uncertainty is always present, even when prices are lower.

And the market doesn’t schedule dips based on our comfort.

Example 2: The automatic investor

Jordan invests $500 every two weeks into a diversified portfolio, no matter what the market is doing. When prices rise, he buys fewer shares.

When prices fall, he buys more. He doesn’t always feel good about it, but he keeps the habit. Over time, his average purchase price reflects

many market environmentsnot one dramatic moment.

Jordan’s superpower isn’t prediction. It’s consistency.

Frequently Asked Questions

“Should I invest a lump sum at an all-time high?”

If your plan is long-term, many investors choose to invest according to their allocation rather than wait for a dip.

If you’re nervous, a phased approach (splitting the amount into several scheduled investments over a few months) can help you commit

without feeling like you’re taking one giant leap on one specific day.

“What if a recession hits right after I buy?”

That’s always a possibility. Recessions and drawdowns are part of the deal. The question is whether your portfolio is built to survive it:

appropriate stock/bond mix, emergency cash, and a time horizon that allows recovery. If you need the money soon, reduce risk. If you don’t,

build a plan you can stick with when it gets uncomfortable.

“Isn’t it smarter to wait in cash or T-bills until things calm down?”

Cash can be useful for near-term goals and peace of mind. But “until things calm down” is tricky, because the market often rallies

while the news still feels terrible. If you hold cash as part of a plan, great. If you hold cash because you’re waiting to feel safe,

be honest: that day may never arrive.

Conclusion: The Market Keeps Setting Records Because Progress Keeps Happening

Record highs feel dramatic because they’re measurable and headline-friendly. But zoom out and they’re normal.

Historically, markets have hit many all-time highs on the way to building long-term wealthoften clustering during strong uptrends.

The most “wealth of common sense” takeaway is simple: don’t let a new high bully you into abandoning a good plan.

Use automation, diversification, rebalancing, and realistic expectations. Let the long-term compounding do the heavy lifting

while you get on with your lifepreferably doing something more fun than staring at a chart like it owes you money.

Experiences at All-Time Highs: What It Actually Feels Like (and What People Learn)

If you’ve never invested through a string of record highs, here’s the weird truth: the first few feel thrilling, then the next few feel suspicious,

and eventually you start treating them like background noiseassuming you survive the emotional obstacle course in the middle.

One common experience is what I’ll call “The Dip Waiter’s Spiral.” This is the investor who wants to be responsible,

so they wait for a pullback that feels “deserved.” They don’t want to be the person who buys the top. The market climbs anyway.

At some point, the Dip Waiter either (a) buys higher, (b) stays in cash and grows increasingly bitter, or (c) discovers index funds and automation

and stops trying to outsmart a crowd of millions. Option (c) is the one that tends to improve sleep quality.

Another experience: the constant “it’s different this time” soundtrack. Every era has a reason the market should not be at a high.

Inflation. Elections. Wars. Tech bubbles. Housing bubbles. Rate hikes. Rate cuts. A yield curve doing yoga poses it shouldn’t be able to do.

The headlines change outfits, but the emotional punchline stays the same: uncertainty feels like a signal, even when it’s just the normal weather of investing.

Then there’s the Automatic Investorthe person who quietly keeps buying through records because the money moves on payday

and the decision has been removed from the weekly mood swing. This investor still feels emotions, but the system is stronger than the emotions.

When friends ask, “Are you buying at these levels?” the Automatic Investor shrugs and says, “I’m buying at all the levels.”

It’s not flashy, but it’s often effective.

A close cousin is the Rebalancer. Record highs for this person are not a reason to panic; they’re a reminder to check the portfolio.

If stocks have grown too large compared with bonds or cash, the Rebalancer trims a little and restores the target mix.

When stocks fall later, the Rebalancer adds back according to the same rules. The emotional experience here is surprisingly calm,

because the investor isn’t trying to predict the marketthey’re trying to control their exposure to it.

Finally, there’s the Reformed Market Timer. Most people who swear off timing didn’t do it because they read one inspirational quote.

They did it because they tried timing, and it punched back. They sold during fear, waited for clarity, and discovered that clarity is usually delivered

after prices have already moved. The reform isn’t moral; it’s practical. They learn that the market doesn’t hand out “certainty coupons.”

So they choose a diversified plan, keep contributions steady, and accept that feeling uneasy is not the same thing as being wrong.

The shared lesson across these experiences is simple: record highs are uncomfortable because they force you to admit you can’t control the next 6 months.

The way through isn’t prediction. It’s preparationtime horizon, diversification, and a process you can repeat when your brain starts composing disaster documentaries.

Research Basis (No Links, Just the Reputable Sources Used)

- A Wealth of Common Sense (Ben Carlson) – historical context on all-time highs and clustering

- Fidelity Learning Center – investing at all-time highs, dollar-cost averaging guidance

- Vanguard research & market outlook materials – valuations, long-term return expectations, investing behavior

- Charles Schwab Education – market timing research and investing during market highs

- J.P. Morgan Asset Management – long-run market participation and “missing best days” illustrations

- Wells Fargo Advisors – volatility, best/worst days proximity, timing risk

- Hartford Funds – historical return context around all-time highs

- Federal Reserve Bank of St. Louis (FRED) – S&P 500 data context

- S&P Dow Jones Indices – index definitions and methodology context

- Associated Press – recent examples of markets reaching record highs

- Reuters – market record-high reporting and drivers (rates, earnings, sentiment)

- MarketWatch – volatility timing risk examples and best/worst day dynamics

- Kiplinger – recent record-high market coverage

- Investopedia – long-run S&P 500 return context and investing concepts

- Yahoo Finance – recent record-high context and investor discussion points