Table of Contents >> Show >> Hide

If you only judge the stock market by headlines, small caps look like the kid who showed up to the party with a homemade dip while the mega-cap tech crowd arrived in a private jet. For years, America’s biggest companies have soaked up attention, performance, and oxygen. Meanwhile, small-cap stocks have spent a long stretch being called disappointing, risky, irrelevant, or, in the most dramatic version of the argument, dead.

That makes for a spicy headline. It also oversimplifies what is really happening.

The better question is not whether small caps are dead. It is whether the old, easy small-cap story is dead. The classic idea was simple: buy smaller companies, wait patiently, and enjoy a long-run “small-cap premium” because smaller businesses tend to grow faster and reward investors for taking more risk. That story has not disappeared, but it has become messier. Market structure has changed. Private capital has changed. Interest rates have changed. Even the definition of “good small cap” has changed.

So no, small caps are not dead. But they are no longer a one-size-fits-all shortcut to outperformance. Today, investing in small caps is less like buying a whole basket of baby Amazons and more like sorting through a flea market where one table hides vintage treasure and the next table is selling broken lamps and deep regret.

This article takes a realistic look at why small caps have struggled, what is still attractive about them, and what investors should understand before declaring the entire asset class deceased.

What Counts as a Small-Cap Stock?

In plain English, small-cap stocks are shares of smaller publicly traded companies. There is no magical market-cap line that the stock market police enforce with whistles, but most investors use major indexes as a practical guide. In the United States, the Russell 2000 and the S&P SmallCap 600 are two of the best-known benchmarks for the space.

That detail matters because not all small-cap indexes are built the same way. The Russell 2000 is broader and captures a huge swath of smaller listed companies. The S&P SmallCap 600 is narrower and includes screens for liquidity and financial viability. In other words, one index is more willing to invite the entire neighborhood, while the other checks whether guests are wearing shoes.

That difference helps explain why investors can have very different experiences with “small caps” depending on what, exactly, they own.

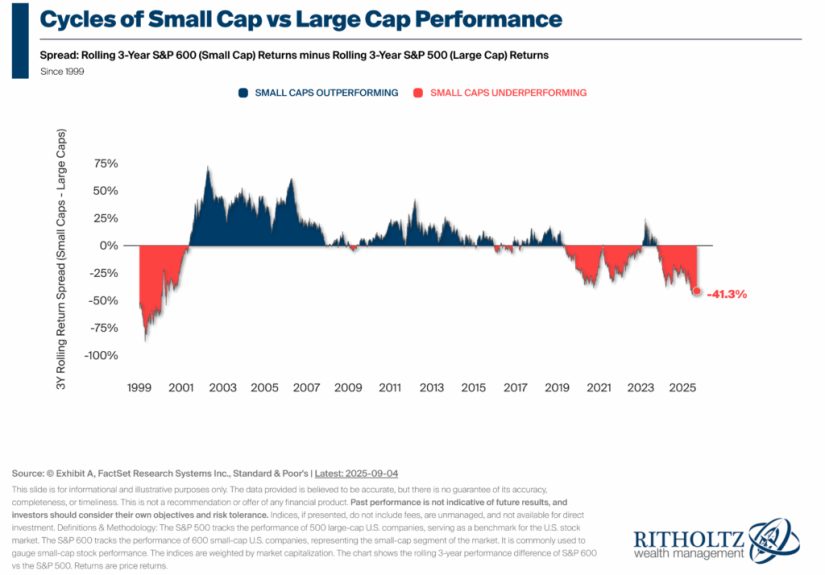

Why So Many People Think Small Caps Are Dead

Mega-Cap Dominance Has Been Ruthless

The first reason small caps feel dead is brutally simple: large caps, especially giant growth stocks, have dominated investor attention. The AI boom, platform economics, strong balance sheets, and massive profit pools have made America’s biggest companies look almost unfairly powerful. When a handful of enormous firms are driving a huge share of market returns, smaller companies can feel invisible.

This kind of concentration creates a psychological trap. Investors stop asking whether small caps are reasonably priced or improving fundamentally. They start asking why they should bother with anything that is not already famous. That usually happens near the peak of a trend, not at the beginning.

Still, the frustration is understandable. Watching small-cap funds trail while large-cap indexes set the tone can make even patient investors feel like they brought a bicycle to a Formula 1 race.

Higher Rates Hit Smaller Firms Harder

Small caps are often more sensitive to interest rates and credit conditions than their larger peers. Many smaller companies borrow at higher costs, have less room for refinancing mistakes, and operate with thinner margins. When money was cheap, that was manageable. When rates rose sharply and stayed restrictive for longer than many investors hoped, small caps faced a rougher road.

The issue is not merely that higher rates make borrowing expensive. It is that they expose weak business models. A large company with strong cash flow can absorb financing pressure. A smaller company that depended on easy credit and optimistic forecasts can suddenly look fragile. That is one reason small-cap performance has often moved closely with expectations around the Federal Reserve, economic growth, and lending conditions.

Even with the effective federal funds rate lower than its 2023 highs, financing conditions still matter. Smaller businesses do not celebrate simply because rates are no longer climbing like a caffeinated squirrel. They need funding conditions that actually support expansion, hiring, and investment.

Private Markets Changed the Old Small-Cap Playbook

Another major shift is structural. Decades ago, many exciting younger companies reached public markets earlier in their life cycles. Investors in public small caps had better access to early-stage growth. Today, private equity, venture capital, and private credit allow companies to stay private longer. By the time some firms list publicly, a big chunk of the explosive growth phase may already be gone.

This change matters more than many casual investors realize. If the most dynamic small businesses are living longer in private markets, public small-cap indexes may contain a lower average quality mix than they once did. Some of the best future stars arrive late. Some promising firms get bought before they ever mature in public view. And some weaker companies remain listed longer than anyone would choose if they were designing the market from scratch.

That does not kill the small-cap opportunity. It does mean the old historical premium may be less automatic than textbooks made it sound.

Small-Cap Indexes Contain Real Junk

This is the uncomfortable part that polite asset allocation slides sometimes whisper instead of saying out loud: some small-cap indexes include a lot of low-quality companies. Not just “temporarily misunderstood future winners,” but genuinely weak businesses with shaky profitability, heavy leverage, poor liquidity, or unclear competitive advantages.

That is one reason the small-cap universe can look worse than the small-cap idea. If an investor buys a broad small-cap product, they are not just buying entrepreneurial grit. They may also be buying debt problems, low margins, inconsistent governance, and business plans that look great only in PowerPoint.

Quality screens, profitability filters, and active selection can make a meaningful difference here. In small caps, what you own matters more than the label on the box.

The Case That Small Caps Are Not Dead

Valuations Look More Reasonable Than in Mega-Cap Land

One of the strongest arguments for small caps is valuation. After years of underperformance, many small-cap shares trade at much less demanding prices than the giant companies that have dominated the benchmark conversation. That does not guarantee a rebound, but it improves the odds that future returns come from something sturdier than pure optimism.

Investors tend to forget that disappointing recent performance can be the seed of better forward returns. Markets do not hand out trophies for what already worked; they price assets based on what comes next. If large caps are already loved, admired, and photographed from their best angles, small caps may benefit simply from lower expectations.

Cheap does not mean safe, of course. Plenty of stocks are cheap for reasons that become painfully obvious later. But broadly speaking, a less stretched starting point gives small caps a better setup than their recent reputation suggests.

Earnings Breadth Can Improve Faster Than Headlines Suggest

Another reason not to bury small caps is that earnings trends can turn before the narrative does. Smaller companies are more cyclical, so their results can improve meaningfully when growth stabilizes, credit pressure eases, or sector breadth widens beyond a handful of market giants.

That matters because markets often behave like terrible dinner guests: they show up early, overreact, and leave before dessert. By the time the average investor hears that small-cap fundamentals are improving, a meaningful part of the move may already be underway.

If earnings breadth expands beyond the narrow leaders that have dominated the tape, small caps can suddenly go from forgotten to fashionable. Markets have done this before, and they can do it again without sending a formal announcement.

Small Caps Are More Tied to the Domestic Economy

Unlike many giant multinational corporations, smaller U.S. companies usually get more of their revenue at home. That makes small caps a more direct way to express a view on the U.S. economy. If domestic demand holds up, business investment improves, or policy becomes more supportive for local operators, small caps can benefit.

That domestic exposure is a double-edged sword. If the U.S. economy weakens sharply, small caps can feel the pain fast. But if investors want exposure to an American growth broadening story rather than just a few global titans, small caps remain one of the clearest places to look.

In other words, small caps are not dead. They are simply less insulated. They are like convertibles in a rainstorm: more fun when the weather cooperates, less charming when conditions turn ugly.

History Rarely Rewards the Most Obvious Trade Forever

Another point worth remembering: no leadership regime lasts forever. Large-cap dominance can persist longer than expected, but markets eventually rotate. Valuation gaps matter. Earnings cycles matter. Sentiment extremes matter. The trade that feels effortless often becomes crowded, expensive, and vulnerable to disappointment.

That does not mean investors should blindly load up on small caps and wait for destiny to arrive wearing a cape. It means the asset class should not be dismissed just because the recent decade has favored bigger companies. The stock market loves making one trend look permanent right before it stops being quite so permanent.

What Investors Get Wrong About Small Caps

They Assume All Small Caps Are the Same

This is probably the biggest mistake. Small caps are not a single personality type. They include industrial firms, banks, niche software companies, retailers, healthcare names, manufacturers, and turnaround stories that could either recover or star in a cautionary tale.

A profitable small-cap industrial company with pricing power is very different from a speculative biotech firm burning cash. A regional bank is very different from a small software firm with recurring revenue. Yet investors often treat the entire category as one blob. That is like saying every restaurant is identical because they all own chairs.

They Think Rate Cuts Automatically Solve Everything

Yes, lower rates can help small caps. But not all small-cap rallies are created equal, and not every rate-cut cycle is a magic cure. If the Fed is easing because growth is collapsing, weaker small companies may still struggle. The best setup for small caps is not simply “rates down.” It is a more nuanced combination of manageable inflation, easing financial conditions, and growth that is soft enough to calm rate pressure but solid enough to support profits.

That is a fancy way of saying small caps do not just need cheaper money. They need usable oxygen.

They Confuse Cheap With Durable

A stock can look statistically cheap and still be a bad business. In small caps especially, low multiples can hide balance-sheet stress, poor management decisions, cyclicality, or industries in decline. The smarter question is not “Is this stock cheap?” but “Is it cheap relative to a business that can actually survive and compound?”

The strongest case for small caps today is not blind bargain hunting. It is selective exposure to companies with healthy balance sheets, credible earnings potential, and room to grow without depending on fantasy financing conditions.

So, Are Small Caps Dead?

No. Small caps are not dead. But the lazy version of the small-cap thesis is on life support.

The old assumption that small caps will automatically outperform because they are smaller is much harder to defend in a world shaped by giant tech platforms, deep private capital markets, profitability gaps, and higher financing sensitivity. The small-cap premium may still exist, but it is less clean, less constant, and more dependent on quality, valuation, and timing than many investors once believed.

That is not bearish. It is realistic.

Small caps still offer traits that matter: lower relative valuations, domestic economic sensitivity, room for earnings acceleration, and the potential for sharp rerating when market leadership broadens. They also carry more landmines than many large-cap benchmarks. That means investors need more discernment than nostalgia.

If you want a neat one-line answer, here it is: small caps are not dead; they are just no longer easy. And honestly, that may be exactly why they still deserve attention.

Experience: What Following the Small-Cap Debate Actually Feels Like

If you have spent any time following small caps over the last few years, the experience is strangely emotional for an asset class that is usually discussed with charts, factors, and very serious eyebrow movements. One month, small caps are “the next big rotation.” The next month, they are “too risky in a higher-rate world.” Then they rally for a few weeks and everybody suddenly remembers they exist. After that, one ugly inflation print or one nervous credit headline comes along, and the entire trade gets shoved back into the closet with last season’s optimism.

For investors, this creates a particular kind of fatigue. Large-cap investing often feels straightforward: own the obvious winners, tolerate the valuation, and let the market admire scale, cash flow, and AI exposure. Small-cap investing feels different. It asks for patience without always offering validation. You can be early for a perfectly good reason and still look wrong for a long time. That experience is hard, especially in an era where every app, headline, and social post tells you exactly which giant stocks are “working” right now.

There is also the experience gap between theory and reality. In theory, small caps are where innovation, inefficiency, and long-term opportunity meet. In reality, they can be volatile, uneven, and occasionally full of companies that make you wonder whether public markets should have a bouncer. That tension is part of the journey. Investors who stay in the space long enough usually stop looking for a glorious, instant comeback and start focusing on process: quality, balance sheets, valuations, and whether earnings are improving beneath the surface.

Another common experience is learning that index choice quietly changes everything. Someone who owns a broad small-cap benchmark may feel like the whole segment is broken. Someone focused on more profitable small companies may have a completely different impression. Two investors can both say, “I own small caps,” while one is holding resilient niche businesses and the other is carrying a backpack full of micro-dramas with ticker symbols.

Perhaps the most revealing experience is psychological. Small caps teach investors what they really believe about markets. Do they only like assets after they become popular? Can they tolerate stretches when the crowd seems uninterested? Can they separate temporary disappointment from permanent impairment? Small caps tend to expose whether someone wants opportunity or just applause.

That is why the question “Are small caps dead?” keeps coming back. It is not only about the companies. It is about investor patience, memory, and discomfort. When large caps dominate, small caps feel unnecessary. When leadership broadens, they suddenly look essential. The experience of owning them is often less about being constantly right and more about being willing to sit through periods when the market acts like size is destiny. It is not comfortable. But that discomfort is often where the real debate begins.

Note: This article is for informational purposes only and does not constitute personalized investment advice.