Table of Contents >> Show >> Hide

Interest rates are the economy’s version of background music. Most people do not notice them until the song gets weird, too loud, or suddenly turns into free jazz at dinner. For the past few years, Americans have heard nonstop talk about the Federal Reserve, rate hikes, rate cuts, mortgage spikes, cooling inflation, and the eternal guessing game known as “What will Jerome Powell do next?” Yet many households and businesses still ask the same practical question: When will interest rates really start to matter?

The honest answer is that interest rates already matter. They matter a lot. But they do not hit everyone at the same time, in the same way, or with the same force. That is why the economy can look oddly calm on the surface while pressure builds underneath. A saver with cash in a high-yield account may feel like rates are a gift. A first-time homebuyer may feel like rates are a brick wall wearing a suit. A business with old low-cost debt may not care much yet, while a family carrying revolving credit card balances is already paying a very expensive price.

So the better question is not whether interest rates matter. It is when they begin to change behavior. That is the moment rates become economically important in a way people can feel in their monthly budget, hiring decisions, investment plans, and spending habits. In other words, rates really start to matter when they stop being headlines and start becoming habits.

Interest Rates Already Matter, Just Unevenly

One reason the debate gets confusing is that interest rates do not move through the economy like a light switch. They work more like a delayed sprinkler system. Some parts get soaked immediately. Others stay dry for a while, then suddenly wonder why the carpet is ruined.

Homebuyers Feel It First

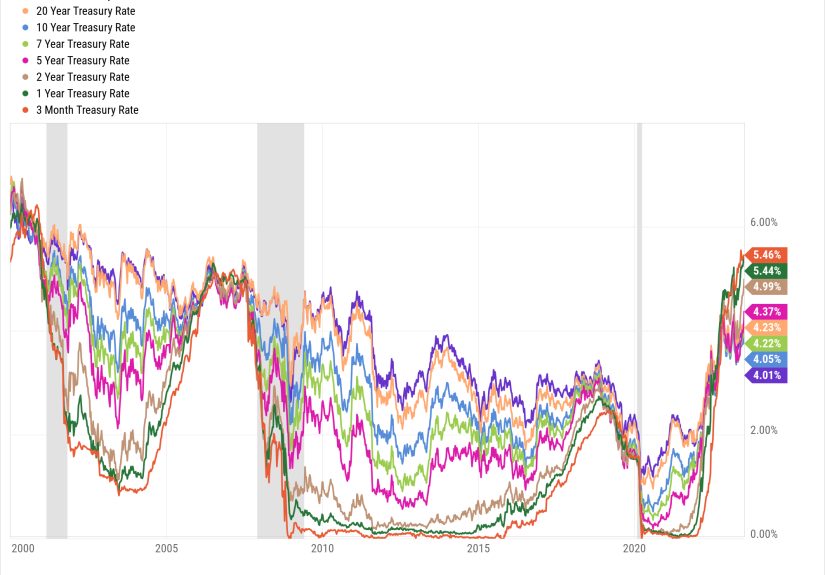

Housing is usually the clearest early warning sign. Mortgage rates react not only to the Fed but also to Treasury yields, inflation expectations, and financial market nerves. That means homebuyers can feel pressure even when the Fed does nothing at all. If mortgage rates jump, affordability changes fast. A small move in rates can mean a large difference in monthly payments, especially at today’s home prices.

That is why housing is often the first place where interest rates “really matter.” They do not just affect spreadsheets. They change who qualifies for a loan, who delays buying, who settles for a smaller house, and who gives up and renews a lease with a deep sigh and a stronger coffee habit.

Credit Card Borrowers Feel It Constantly

Credit cards are where high rates become painfully personal. Unlike a fixed-rate mortgage locked in years ago, revolving debt keeps reminding borrowers that money is not free and banks are not charities. When average card APRs stay elevated, carrying a balance gets more expensive every month. The effect is not dramatic in a cinematic way. It is worse. It is repetitive. Quiet. Annoying. It eats cash flow one billing cycle at a time.

That is why many consumers do not need a recession to feel restrictive monetary policy. They just need a statement balance, a minimum payment, and the rude awakening that interest has become a permanent roommate.

Savers Benefit, but Not Equally

Higher rates also create winners. Savers with cash can earn much more than they could during the near-zero-rate era. High-yield savings accounts, CDs, and money market accounts became meaningful again. For households with emergency funds or retirees relying on safer income, that has been a real improvement.

Still, the gain is uneven. Big traditional banks often pay very little compared with top online accounts. So even when rates rise, many consumers do not benefit unless they move their money. In plain English: the rate environment may be generous, but your bank might still be acting like it is 2019 and doing you a favor with 0.01%.

Why the Full Economic Impact Takes Time

If rates are so powerful, why does the broader economy sometimes seem slow to react? Because much of modern finance is built around time delays. Households refinance. Companies roll debt. Landlords renew leases. Businesses hedge costs. Consumers postpone choices. Monetary policy is not a hammer that lands all at once. It is a tightening coil.

Fixed-Rate Debt Delays the Pain

Millions of homeowners refinanced or bought homes when mortgage rates were much lower. As long as they keep those loans, their monthly payment does not change. That helps explain why the housing market can freeze without instantly collapsing. Existing owners stay put. New buyers struggle. Inventory changes slowly. Rates matter, but the pain shows up in transactions and affordability before it appears in widespread household distress.

Businesses Often React Late

Many companies do not borrow every quarter. Some raised cash earlier, locked in lower-cost debt, or have enough balance-sheet strength to absorb higher interest expense for a while. That delay matters. Rate pressure often shows up later through reduced expansion plans, delayed hiring, weaker capital spending, and tighter financial conditions.

When borrowing costs stay high long enough, finance teams stop asking, “Can we fund this project?” and start asking, “Do we really need this project?” That is the pivot point. It may not make headlines immediately, but it affects productivity, hiring, wage growth, and eventually consumer demand.

The Labor Market Acts Like a Shock Absorber

Interest rates become much more important when the labor market weakens. As long as people are working, wages are still rising, and layoffs are limited, households can often absorb higher borrowing costs longer than expected. That is one reason central banks watch employment so closely. A strong labor market can cushion higher rates. A softer labor market can amplify them.

When job growth slows, unemployment drifts higher, and workers become less confident about future pay, higher rates go from “annoying” to “behavior-changing.” Consumers spend less. They borrow less. They delay moves, travel, renovations, and bigger purchases. Businesses notice. Then they pull back too. That is when interest rates truly start to matter across the wider economy.

So, When Do Interest Rates Really Start to Matter?

They really start to matter when three things happen at once: borrowing stays expensive for long enough, income growth stops offsetting the cost, and confidence begins to crack.

That point does not arrive on the day the Fed raises or cuts rates. It arrives when the effects spread from financial markets into everyday decisions. Here is what that usually looks like in real life.

1. When Monthly Payments Change What People Can Buy

The first real threshold is affordability. If a higher mortgage rate prices a buyer out of a neighborhood, rates matter. If an auto loan pushes a monthly payment above the budget, rates matter. If a card balance takes longer to pay down because more of the payment goes to interest, rates matter. This is not abstract economics. It is a kitchen-table rewrite of what is possible.

2. When Refinancing Stops Saving People

In low-rate years, households and firms could refinance debt, lower monthly payments, and free up cash. In a higher-rate environment, that release valve closes. Suddenly, there is less room to shuffle obligations into something cheaper. Consumers lose flexibility. Businesses lose optionality. That is when tighter policy becomes stickier.

3. When Employers Turn Cautious

Rates become far more important once they influence hiring plans. A company does not need to be in trouble to freeze hiring. It just needs to become uncertain enough. If financing is expensive, demand is wobbling, and future inflation looks murky, many executives decide to wait. And when enough businesses wait at the same time, the economy slows in a way households can feel.

4. When People Stop Assuming Relief Is Coming

Expectations matter. If consumers and investors believe rate cuts are just around the corner, they may keep spending, borrowing, and investing with more confidence. But if markets begin to think rates will stay higher for longer, behavior changes before policy does. That is one reason bond yields, mortgage rates, and credit conditions can tighten even when the Fed holds steady. Markets do not wait politely for the official memo.

What the Current Economy Suggests

Right now, the U.S. economy offers a mixed picture. Inflation has cooled substantially from its peak, but it is still not perfectly settled. Growth has slowed. The labor market looks softer than it did when the economy was running hot, yet it has not cracked wide open. That combination makes the timing question more important than ever.

In practical terms, interest rates are already biting in the most rate-sensitive corners of the economy. Housing affordability remains strained. Mortgage activity responds quickly when long-term yields jump. Credit card debt is expensive. Consumers carrying balances feel the squeeze every month. Businesses facing new financing decisions are more cautious than those still living off older low-cost debt.

At the same time, rates have not fully crushed the broader economy because households still have some resilience, higher-income consumers still spend, and savers are earning more on cash. That helps explain why the economy can slow without immediately falling apart. It is not that rates do not matter. It is that the transmission is uneven and incomplete.

Recent data point to exactly this kind of in-between moment. Inflation is lower than it was at its worst, but still above the Fed’s comfort zone. Economic growth has cooled sharply from stronger quarters. Employment has softened without imploding. In that setting, the key issue is duration. If borrowing costs remain elevated and inflation risks keep rate cuts on hold longer than expected, the cumulative effect will matter more than any single Fed meeting.

The Areas to Watch Next

If you want to know when interest rates will really matter in a bigger, economy-wide way, watch five things.

Housing Turnover

Not just home prices, but how many people are actually buying, selling, refinancing, or staying stuck. A frozen housing market is one of the clearest signs that rates are changing behavior.

Delinquency Trends

Credit card, auto loan, and student loan stress can reveal where households are running out of breathing room. Rising delinquencies often show that rates are no longer just expensive. They are becoming unsustainable for part of the population.

Business Investment

When capital spending weakens, it is often a sign that financing costs are biting harder than headline GDP suggests. Fewer projects today can mean slower productivity and weaker job growth tomorrow.

Hiring and Wage Growth

As long as incomes are rising and jobs remain available, consumers can keep navigating high rates. If job growth weakens further, the same interest-rate level suddenly feels much heavier.

Consumer Psychology

This one sounds fuzzy, but it matters. When people stop believing next quarter will be easier, they become more defensive. That is how “higher rates” turns into “I am not making that purchase right now.” Enough of those decisions add up fast.

Real-World Experiences: When Rates Stop Being Theory and Start Running the Room

To understand the topic more clearly, it helps to look at lived experiences rather than policy jargon. Consider the first-time homebuyer who spent months watching listings, calculating down payments, and waiting for the “right moment.” On paper, a difference of one percentage point in mortgage rates may not sound life-changing. In reality, it can wipe out an entire slice of the buyer’s budget. That does not just change the house they can afford. It changes the school district, the commute, the renovation plans, and the timeline for starting a family. For that buyer, interest rates started to matter long before any economist announced a broader slowdown.

Now think about a household carrying credit card debt after a year of stubborn grocery bills, car repairs, and a few medical expenses. They may still be employed. They may still look financially “fine” from the outside. But when the interest portion of the monthly payment gets large enough, the balance stops shrinking in a meaningful way. The family cuts restaurant spending, pauses a vacation, and delays replacing an aging appliance. Nothing dramatic happens in a single day. Yet the household has already shifted into defensive mode. Rates matter because they are quietly changing daily life.

Small-business owners often experience the same pressure from a different angle. A local company may have survived inflation, supply issues, and higher wages, but now faces the cost of renewing a credit line or financing new equipment. The owner does not necessarily cancel growth plans out of panic. Instead, they become selective. Hiring one more employee turns into waiting a quarter. Opening a second location becomes “maybe next year.” A software upgrade gets postponed. That hesitation is exactly how higher rates slow the economy: through accumulated caution.

Savers, of course, can have the opposite experience. Someone who kept a healthy emergency fund during the near-zero-rate era may finally feel rewarded. Earning meaningful yield on cash can reduce anxiety and strengthen financial discipline. Retirees, conservative investors, and households building a down payment may welcome higher rates because safe money is paying something again. But even that experience contains a twist. Savers who leave cash at a low-paying traditional bank may not feel much benefit at all, which shows that rate policy and actual consumer outcomes are not always the same thing.

The broad lesson from these experiences is simple: interest rates really start to matter when they alter choices, not just headlines. They matter when someone buys less house, pays debt longer, delays hiring, chooses savings over spending, or decides uncertainty is reason enough to wait. That is why the most important impact of interest rates is often not visible in a single chart. It lives inside thousands of ordinary decisions made by households and businesses trying to stay flexible in an economy where money suddenly has a more noticeable price tag.

Conclusion

So, when will interest rates really start to matter? For many Americans, they already do. But in the broader economy, they matter most when high borrowing costs last long enough to change behavior across housing, consumer debt, business investment, and hiring. That is the real tipping point. Not the press conference. Not the market rumor. Not the social media economist with a dramatic chart and too much confidence.

The next phase depends less on whether rates move a quarter point and more on how long financial conditions stay restrictive while growth cools. If inflation stays sticky and rate relief keeps getting delayed, the impact will widen. If inflation eases further and financing costs come down gradually, the economy may absorb the pressure without a major crack. Either way, the lesson is the same: interest rates matter when they stop being background noise and start rewriting what people feel comfortable doing with their money.